事件回测的最大好处是基本上可以避免未来函数的出现。

代码如下:

3 | from __future__ import division |

11 | data = ts.get_hist_data("510050",start="2017-01-01",end="2017-09-08") |

12 | data = data.sort_values("date") |

14 | df['close'] = data['close'] |

15 | df['change'] = df['close']- df['close'].shift(1) |

16 | df = df.dropna() #将带有Na的去掉,返回一个新的对像 |

18 | close5_array = np.zeros(5) #缓存过去5天收盘价 |

19 | close20_array = np.zeros(20) |

20 | last_signal = 0 #最近交易信号,初始化为0。因为双均线策略要使用前一天的收盘价,就需要将信号缓存下来,第2天计算仓位的时候使用 |

21 | last_pos = 0 #最近的持仓,初始化为0 |

32 | self.last_pos = 0 #昨日持仓 |

38 | def calculate(self,date,close,change, last_signal, last_pos): |

44 | self.pos = last_signal |

45 | self.last_pos = last_pos |

48 | self.pnl = self.change * self.pos |

49 | self.fee = abs(self.pos-self.last_pos) * 1.5/10000 |

50 | self.net_pnl = self.pnl - self.fee |

53 | #iterrows生成迭代器,enumerate在迭代过程中返回当前的变量的计数情况。df刚好有date, close, change三列。叠代过程中会以tuple的形式返回每一行,其中的第一个元素是日期,第二个元素是数值段。 |

54 | for i, row in enumerate(df.iterrows()): |

56 | close =row[1]['close'] |

57 | change = row[1]['change'] |

60 | close5_array[0:4] = close5_array[1:5] |

61 | close20_array[0:19] = close20_array[1:20] |

64 | close5_array[-1] = close |

65 | close20_array[-1] = close |

67 | #如果尚未有20个数据点的缓存数量,则不执行后续逻辑 |

73 | dr.calculate(date, close, change, last_signal,last_pos) |

81 | ma5 = close5_array.mean() |

82 | ma20 = close20_array.mean() |

89 | result_df = pd.DataFrame() |

90 | result_df['net_pnl'] = [dr.net_pnl for dr in dr_list] #将dailyresult列表中的数据转换为pandas的dataframe |

91 | result_df.index = [dr.date for dr in dr_list] #添加日期索引 |

93 | result_df['cum_pnl'] = result_df['net_pnl'].cumsum() #累积求和 |

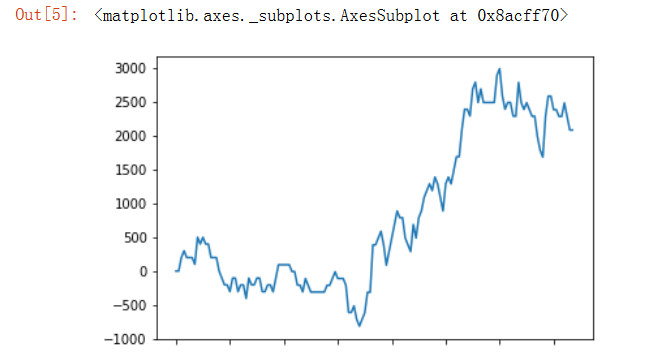

94 | result_df['cum_pnl'].plot() |

在jupyter运行结果如下: